#Module Level Power Electronics Market opportunity

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

70% of Tumblr users say the Dashboard is their favorite place to spend time online.

Text

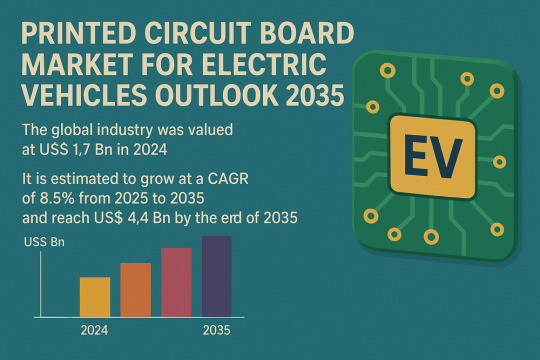

Smart Mobility Drives Smart PCBs: Market to Hit $4.4Bn by 2035

The global Printed Circuit Board (PCB) Market for Electric Vehicles (EVs) is set to witness significant expansion over the next decade, according to the latest market analysis. Valued at US$ 1.7 billion in 2024, the market is projected to grow at a CAGR of 8.5% from 2025 to 2035, reaching a valuation of US$ 4.4 billion by the end of the forecast period.

Market Overview: Printed Circuit Boards (PCBs) are the electronic backbone of electric vehicles, enabling power distribution, connectivity, and control across critical systems such as battery management, motor control, infotainment, and advanced safety features. With EV adoption accelerating globally, PCBs have become essential to the performance, reliability, and innovation of next-generation vehicles.

Market Drivers & Trends

One of the primary drivers of this market is the growing investment and strategic partnerships in the EV supply chain. Leading automakers and electronics companies are heavily investing in R&D and manufacturing capacity to meet the increasing demand for high-performance PCBs.

Moreover, the rise of autonomous and connected vehicles has made sophisticated electronics an indispensable part of modern transportation. The proliferation of features like ADAS (Advanced Driver-Assistance Systems), V2X communication, and in-vehicle infotainment is pushing the demand for compact, multi-layer, high-speed, and thermally efficient PCBs.

In 2023, EV sales in the U.S. surged by 60%, while the European Commission invested over US$ 6 billion in EV infrastructure further stimulating demand for advanced PCB solutions.

Latest Market Trends

The industry is witnessing a rapid shift toward flexible and high-density interconnect (HDI) PCBs, which are crucial for compact and space-saving vehicle designs. Flexible PCBs, in particular, are gaining traction in battery management systems and advanced sensor modules due to their lightweight and adaptable nature.

Additionally, regulatory advancements such as the FCC's allocation of the 5.9 GHz band for vehicle safety and autonomous functions have opened doors for new PCB capabilities. Real-time, high-speed data transmission requires advanced PCB materials and multi-layer configurations.

Key Players and Industry Leaders

Some of the most prominent players shaping the global printed circuit board market for electric vehicles include:

ABL CIRCUITS

AT&S Austria Technologie & Systemtechnik Aktiengesellschaft I

Chin Poon Industrial Co., Ltd.

Compeq Manufacturing Co., Ltd.

HannStar Board Corporation

Kinwong Electronic Co. Ltd

LG Innotek

MEIKO ELECTRONICS Co., Ltd.

Nan Ya Printed Circuit Board Corporation

RayMing PCB

Rush PCB Ltd.

SCHWEIZER ELECTRONIC AG

Shenzhen Capel Technology Co., Ltd.

Shenzhen Fastprint Circuit Tech Co., Ltd.

TTM Technologies

Unimicron Technology Corporation

Victory Giant Technology Co., Ltd.

WUS Printed Circuit Co., Ltd.

Young Poong Group

Zhen Ding Tech. Group

Among Others

These companies are prioritizing innovation, expanding global manufacturing footprints, and forging strategic alliances to maintain competitiveness and cater to evolving industry needs.

Download now to explore primary insights from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=86464

Recent Developments

October 2024 – Mektech Manufacturing announced a 920 million baht investment in Thailand to expand production capacity for flexible PCBs and FPCBA used in electric vehicles.

July 2024 – Omron Electronic Components Europe launched a high-power PCB relay for Level 2 EV charging stations. The innovation features double-break contact designs, enabling reduced heat dissipation and enhanced energy efficiency.

Market Opportunities

The market is poised for significant opportunities, particularly in:

OEM collaborations to co-develop application-specific PCBs for power electronics and smart mobility.

Flexible PCB technology, which is expected to revolutionize EV design with lightweight, customizable circuit boards.

Geographical expansion into regions like South Asia and Latin America, where EV adoption is accelerating, and supply chains are emerging.

Additionally, the ongoing reshoring of PCB manufacturing in regions such as North America and Europe presents untapped potential for local players.

Future Outlook

According to analysts, the convergence of EV electrification, autonomy, and connectivity will demand ever more sophisticated PCB solutions. Next-generation EVs will require PCBs capable of managing 50 Gbps data speeds, robust thermal management, and high signal integrity. Flexible, multilayer, and ceramic PCBs are expected to gain ground rapidly.

As regulations around emissions and vehicle safety become more stringent, automakers will rely heavily on advanced PCB solutions to remain compliant and competitive. From battery optimization to smart in-vehicle systems, the demand for high-performance PCBs is set to skyrocket.

Market Segmentation

The global PCB market for EVs is segmented across several parameters:

By Type: Multilayer (dominant with 73.98% market share in 2024), Double-sided, Single-sided

By Substrate Type: HDI/Micro-via/Build-up, Flexible, Rigid-flex, Rigid 1-2 Sided

By Material: FR4, Metal-Based, Ceramic, PTFE, Power Combi-boards

By Application: ADAS, Battery Management, Powertrain, Lighting & Display, Charging, Connectivity, etc.

By Vehicle Type: Passenger Cars, Buses, Two-Wheelers, Trucks, Off-Highway Vehicles

By End Users: OEMs, Tier 1 & 2 Suppliers, Aftermarket

Regional Insights

East Asia is the undisputed leader in the global market, accounting for 68.3% of the total share in 2024. The region’s dominance stems from:

A well-established electronics manufacturing ecosystem

Government support for EV expansion and green technology

Cost-effective production and high R&D capabilities

Japan, South Korea, and China house the majority of leading PCB suppliers and EV component manufacturers. Their early investment in automation and material innovation is positioning East Asia as the global hub for EV electronics.

Other key regions include:

North America, driven by government initiatives like the CHIPS Act

Europe, focused on sustainable manufacturing and reducing supply chain reliance on Asia

South Asia, emerging as a low-cost, high-volume manufacturing zone

Why Buy This Report?

This in-depth industry report offers:

Detailed market sizing and forecast (2020–2035)

Comprehensive segmentation across product, material, vehicle type, and region

Competitive landscape with profiles of 20+ leading companies

Insights into trends, innovations, and regional dynamics

Strategic recommendations for stakeholders, investors, and policymakers

Whether you're an investor, OEM, component supplier, or policy planner, this report serves as a strategic guide to understanding growth dynamics and identifying emerging opportunities in the PCB market for electric vehicles.

Explore Latest Research Reports by Transparency Market Research: Active Optical Cable Market: https://www.transparencymarketresearch.com/active-optical-cables.html

3D Cameras Market: https://www.transparencymarketresearch.com/3d-cameras-market.html

Optoelectronics Market: https://www.transparencymarketresearch.com/optoelectronics-market.html

Machine Safety Market: https://www.transparencymarketresearch.com/machine-safety-market.html

DC-DC Converter OBC Market: https://www.transparencymarketresearch.com/dc-dc-converter-obc-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Transforming Operations with SAP Supply Chain Management

In today's fast-paced and globally connected market, businesses must have agile, responsive, and data-driven supply chains to remain competitive. One of the most powerful tools helping organizations achieve this is SAP Supply Chain Management (SAP SCM). SAP SCM is an advanced solution designed to optimize and integrate every component of the supply chain, enabling businesses to deliver products efficiently, minimize costs, and enhance customer satisfaction.

What is SAP Supply Chain Management?

SAP SCM is part of SAP’s broader suite of enterprise resource planning (ERP) tools. It offers end-to-end visibility and coordination acrosTransforming Operations with SAP Supply Chain Managements all aspects of the supply chain — from planning and sourcing to manufacturing and delivery. By integrating real-time data, predictive analytics, and intelligent automation, SAP SCM allows companies to better forecast demand, manage inventory, streamline logistics, and respond proactively to market changes.

Key Features of SAP SCM

Supply Chain Planning: SAP SCM provides robust tools for demand forecasting, production planning, and capacity management. Its predictive capabilities allow companies to plan resources effectively and reduce overproduction or stockouts.

Supply Chain Execution: This includes modules for warehouse and transportation management, enabling real-time tracking and coordination of goods movement. It helps reduce delivery delays and improves efficiency.

Collaboration: SAP SCM supports seamless collaboration between suppliers, manufacturers, and customers through shared data and integrated workflows. This helps enhance responsiveness and agility.

Analytics and Insights: SAP’s built-in analytics tools help monitor performance, identify bottlenecks, and uncover opportunities for cost savings or service improvements.

Automation and AI Integration: SAP SCM integrates artificial intelligence (AI) and machine learning (ML) to automate routine tasks and offer smart decision-making support.

Benefits of SAP SCM

Implementing SAP Supply Chain Management offers several strategic advantages:

Enhanced Visibility: Real-time data helps businesses make faster, more informed decisions.

Cost Efficiency: By optimizing inventory levels and reducing waste, SAP SCM significantly cuts down operational costs.

Risk Mitigation: With scenario planning and risk analysis features, companies can better prepare for disruptions.

Scalability: SAP SCM can be tailored to fit businesses of all sizes and is scalable as companies grow.

Sustainability: Improved resource management and optimized logistics contribute to more sustainable operations.

Real-World Applications

From manufacturing to retail and logistics, businesses in various sectors use SAP SCM to streamline operations. For instance, a global electronics manufacturer might use it to balance supply and demand across multiple continents, while a retailer can ensure timely restocking and accurate demand forecasting during peak seasons.

Conclusion

SAP Supply Chain Management is more than just a software solution—it's a strategic tool that transforms how companies operate in a dynamic global environment. By integrating key supply chain functions and enabling smarter decisions through data, SAP SCM empowers organizations to build more resilient, efficient, and customer-centric operations.

Whether you're looking to reduce costs, enhance agility, or drive growth, SAP SCM provides the tools and insights needed to make your supply chain a competitive advantage.

0 notes

Text

Glass Interposers Market 2025

The global glass interposers market was valued at US dollars two hundred thirty four point five million in two thousand twenty four and is forecasted to reach US dollars four hundred seventy eight point nine million by two thousand thirty reflecting a compound annual growth rate of twelve point six percent from two thousand twenty four to two thousand thirty. Glass interposers are innovative interconnection substrates used primarily in advanced semiconductor packaging. These components serve as a bridge connecting multiple integrated circuit dies in high density electronic packages. Unlike traditional interposers made from silicon or organic materials glass interposers utilize ultra thin sheets of specialized glass. Their key advantages include excellent electrical insulation minimal signal loss high thermal resistance and support for fine pitch interconnects. These features make them ideal for high performance computing systems fifth generation telecommunications optoelectronics and advanced consumer electronics.

Get free sample of this report at : https://www.intelmarketresearch.com/semiconductor-and-electronics/864/Glass-Interposers-Market

Glass interposers are essential for packaging technologies such as two point five dimensional and three dimensional integrated circuits where multiple chips are stacked or placed side by side. Their compatibility with through glass vias further enhances high speed data transmission with minimal latency and low power consumption. Glass interposers are well suited for use in artificial intelligence processors data centers and photonic devices because they offer superior electrical insulation thermal stability and higher interconnect density than conventional substrates. Adoption is driven by the push for advanced two point five dimensional and three dimensional packaging technologies and heterogeneous integration.

Market Size On a regional level the United States glass interposers market is also growing robustly. Valued at US dollars sixty one point five million in two thousand twenty four it is projected to reach US dollars one hundred twenty two point three million by two thousand thirty with a compound annual growth rate of twelve point one percent during the same period.

This growth trajectory is driven by the increasing adoption of high performance computing systems advancements in artificial intelligence and fifth generation technologies and the rising demand for miniaturized high density semiconductor packaging.

Market Dynamics Drivers Restraints Opportunities and Challenges Drivers Miniaturization of Electronic Components The trend toward smaller more powerful electronic devices necessitates compact yet high performance packaging. Glass interposers offer the density thermal management and fine line interconnection capabilities that enable this miniaturization.

High Performance Computing and Artificial Intelligence Artificial intelligence and high performance computing workloads require faster data transfer and better thermal management. Glass interposers provide low electrical resistance and superior thermal properties facilitating the performance required in servers graphics processing units and artificial intelligence processors.

Advancements in Semiconductor Packaging With the evolution of two point five dimensional and three dimensional integrated circuit packaging the role of interposers has become more significant. Glass interposers support high density interconnects better signal integrity and can be manufactured to thinner specifications than silicon.

Demand in Consumer Electronics Devices like smartphones wearables and smart home systems increasingly demand efficient space saving packaging. Glass interposers allow the integration of multiple functionalities into a single compact module.

Restraints High Manufacturing Costs The precision and specialized techniques required for producing glass interposers make them costlier compared to alternatives. The capital investment for equipment like laser drilling systems and plasma etching machines is significant.

Complexity in Mass Production Due to the need for ultra thin defect free glass and complex through glass via processing scaling up production remains a challenge.

Availability of Alternatives Silicon and organic interposers are well established in the market with mature production ecosystems and cost advantages. These pose a barrier to wider adoption of glass interposers especially in cost sensitive applications.

Opportunities Fifth Generation and Automotive Electronics Emerging applications in fifth generation infrastructure and automotive electronics require high speed reliable data transmission and thermal stability areas where glass interposers excel.

Material Innovation Integrating glass interposers with new semiconductors photonics and quantum computing components could enable cutting edge innovations in electronics.

Collaborative Development Partnerships between semiconductor manufacturers and glass substrate developers are fostering innovation improving yields and driving down costs.

Challenges Technical Limitations Despite their benefits glass interposers face technical hurdles in areas like ultra high density interconnects and extreme thermal environments.

Market Education and Adoption Shifting from traditional packaging methods requires significant investment and technical training. Convincing manufacturers to adopt glass interposers can be slow.

Supply Chain Bottlenecks The niche nature of the glass interposer market results in a less robust supply chain. Delays in sourcing raw materials or equipment can impact production timelines and costs.

Regional Analysis North America North America particularly the United States is a major player in the glass interposer market driven by high investments in semiconductor research and development and the presence of key technology firms. The strong demand for artificial intelligence cloud computing and fifth generation applications propels regional market growth.

Europe European countries such as Germany the United Kingdom and France are contributing through innovations in automotive electronics and smart industrial systems. Europe’s strong automotive and aerospace sectors also encourage the adoption of advanced interposer technologies.

Asia Pacific Asia Pacific led by China Japan and South Korea dominates the global market in volume. The region houses major semiconductor manufacturers and experiences rapid growth in electronics telecommunications and automotive sectors. Government support and technological advancement in manufacturing processes are also key enablers.

South America and the Middle East and Africa While relatively nascent South America and the Middle East and Africa regions are expected to grow due to increasing mobile and internet penetration smart city initiatives and investments in digital infrastructure.

Competitor Analysis Leading companies in the glass interposers market include

Kiso Micro Co Specializes in ultra thin glass and precision microfabrication Plan Optik AG Known for its high quality glass substrates and microstructured glass Ushio A key supplier of optical and semiconductor equipment Corning Offers specialty glass and ceramic materials with applications in semiconductor packaging Three D Glass Solutions Inc Focused on glass based RF and microwave interposer technology Triton Microtechnologies Inc Provides custom solutions in glass interposer design and manufacturing

These players are engaged in research and development activities strategic partnerships and capacity expansions to enhance their market presence.

Recent Developments In two thousand twenty four through the Packaging Applications Center of Excellence PACE Onto Innovation and LPKF Laser and Electronics SE partnered to expedite the mass manufacturing of glass core based panel level packages. The goal of this partnership is to satisfy the increasing need for cloud computing artificial intelligence and high performance computing applications. Between two thousand twenty five and two thousand twenty six AMD plans to use glass substrates in its high performance system in packages. Advanced system in packages in data center applications can benefit from glass substrates’ superior flatness mechanical strength and thermal characteristics over conventional organic substrates.

Global Glass Interposers Market Segmentation Analysis This report provides deep insight into the global glass interposers market covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size competitive landscape development trend niche market key market drivers and challenges SWOT analysis value chain analysis and more.

The analysis helps the reader to shape competition within industries and to develop strategies for the competitive environment to enhance potential profit. Furthermore it provides a framework for evaluating and assessing the position of the business organization. The report structure also focuses on the competitive landscape of the global glass interposers market. It introduces in detail the market share market performance product situation operation situation and more of the main players which helps industry readers identify the main competitors and deeply understand the competition pattern of the market.

In a word this report is a must read for industry players investors researchers consultants business strategists and all those who have any kind of stake or plan to enter the glass interposers market in any manner.

Market Segmentation by Type Two Dimensional Two point Five Dimensional Three Dimensional

Market Segmentation by Manufacturing Process Laser Drilling and Etching Wafer Level Packaging Temporary Bonding and Debonding Others

Market Segmentation by Application Logic Imaging and Optoelectronics Memory MEMS and Sensors LED Others

Market Segmentation by End Use Industry Consumer Electronics Telecommunications Automotive Healthcare Military and Aerospace Others

Key Companies Kiso Micro Co Plan Optik AG Ushio Corning Three D Glass Solutions Inc Triton Microtechnologies Inc

Geographic Segmentation North America including USA Canada and Mexico Europe including Germany UK France Russia Italy and Rest of Europe Asia Pacific including China Japan South Korea India Southeast Asia and Rest of Asia Pacific South America including Brazil Argentina Colombia and Rest of South America The Middle East and Africa including Saudi Arabia UAE Egypt Nigeria South Africa and Rest of MEA

Frequently Asked Questions FAQs What is the current market size of the Glass Interposers Market As of two thousand twenty four the global glass interposers market is valued at US dollars two hundred thirty four point five million with projections to reach US dollars four hundred seventy eight point nine million by two thousand thirty.

Which are the key companies operating in the Glass Interposers Market Key players include Kiso Micro Co Plan Optik AG Ushio Corning Three D Glass Solutions Inc and Triton Microtechnologies Inc.

What are the key growth drivers in the Glass Interposers Market Growth is fueled by miniaturization of electronics demand for high performance computing advancements in semiconductor packaging and increasing use in consumer electronics.

Which regions dominate the Glass Interposers Market Asia Pacific leads the market in terms of volume while North America is a major player in innovation and adoption. Europe also shows strong growth in automotive and industrial electronics.

What are the emerging trends in the Glass Interposers Market Emerging trends include integration with fifth generation and automotive electronics development of glass photonic interposers and strategic partnerships aimed at cost reduction and innovation.

Get free sample of this report at : https://www.intelmarketresearch.com/semiconductor-and-electronics/864/Glass-Interposers-Market

0 notes

Text

Antenna in Package AiP Market Opportunities Rising with Expansion of Millimeter Wave Technology Globally

The Antenna in Package (AiP) market is gaining significant traction as wireless communication technologies become increasingly integrated into compact, high-performance electronic devices. AiP technology incorporates antennas directly into semiconductor packages, enabling advanced radio frequency (RF) performance while saving space. This innovation is particularly relevant in 5G, millimeter-wave (mmWave), automotive radar, satellite communications, and IoT applications.

Market Drivers

One of the primary drivers of the AiP market is the global rollout of 5G technology, which operates at higher frequencies such as mmWave. These frequencies require advanced antenna solutions capable of handling high data rates and low latency. Traditional printed circuit board (PCB) antennas often fall short in terms of integration and performance. AiP offers a more efficient alternative by reducing interconnect losses and supporting beamforming technologies critical for 5G.

Another major factor is the increasing miniaturization of consumer electronics. Smartphones, wearables, and IoT devices demand compact components that deliver excellent performance. AiP technology meets this requirement by integrating the antenna and RF front-end into a single compact module, freeing up space and improving system-level efficiency.

Technological Advancements

Recent advancements in substrate materials, system-in-package (SiP) technologies, and 3D packaging are making AiP solutions more cost-effective and scalable. Low-temperature co-fired ceramic (LTCC) and organic substrates have enabled better thermal and electrical performance. Integration of multiple functions such as filters, power amplifiers, and transceivers within the package has allowed manufacturers to create multi-functional modules tailored for specific end-uses.

In addition, the evolution of advanced simulation tools and design automation has shortened development cycles and reduced costs, making AiP more accessible to a broader range of industries. These advancements have facilitated faster prototyping and more reliable testing environments.

Key Market Segments

The AiP market can be segmented based on frequency band, end-user application, and geography.

By frequency, the market includes sub-6 GHz and mmWave segments, with mmWave seeing higher growth due to its necessity in 5G and automotive radar applications.

By application, the market is divided into consumer electronics, automotive, telecommunications, aerospace and defense, and industrial IoT.

Geographically, North America and Asia-Pacific dominate the AiP landscape, thanks to the presence of major semiconductor companies and 5G infrastructure deployment.

Regional Insights

Asia-Pacific leads the AiP market due to robust electronics manufacturing ecosystems in countries like China, South Korea, Taiwan, and Japan. Government initiatives to boost 5G and smart city projects further support AiP growth in the region. North America, especially the United States, sees significant demand from telecom providers, defense contractors, and autonomous vehicle manufacturers. Europe is also emerging as a key region, driven by automotive and industrial automation applications.

Competitive Landscape

The AiP market is highly competitive, with key players including Qualcomm, ASE Group, Amkor Technology, Murata Manufacturing, TSMC, and MediaTek. These companies are investing in research and development to improve integration, reduce power consumption, and enhance RF performance. Collaborations, joint ventures, and strategic acquisitions are common strategies to gain market share and accelerate product development.

Startups and mid-sized players are also entering the space with niche AiP solutions for IoT and wearable devices, contributing to market dynamism and innovation.

Challenges and Opportunities

Despite its promise, AiP adoption faces several challenges. High design complexity, thermal management issues, and initial manufacturing costs are significant barriers. Additionally, maintaining signal integrity in densely packed modules remains a technical hurdle.

However, opportunities abound. As mmWave adoption expands and edge computing grows in importance, AiP is poised to play a pivotal role in enabling low-latency, high-speed communication across various devices and systems. The trend toward smart cities, connected vehicles, and AR/VR applications also offers long-term growth potential.

Future Outlook

The AiP market is expected to grow at a CAGR exceeding 15% over the next five years, driven by surging demand across multiple industries. Technological advancements, cost optimization, and expanding 5G infrastructure will be key enablers. As device manufacturers strive to balance performance, size, and power efficiency, AiP is likely to become a standard in RF design and packaging.

#AntennaInPackage#AiPMarket#5GTechnology#MillimeterWave#WirelessCommunication#IoTDevices#RFTechnology

0 notes

Text

Top Innovative STEM Lab Solutions for Schools and Colleges in 2025

In the ever-changing academic environment of today, education has no longer stayed tethered to books and lectures. Because of the real world, schools, colleges, and training institutions are heavily investing in Innovative STEM Lab Solutions to provide a balance between theory and practice. These modern setups have allowed students to hone their scientific, technological, engineering, and mathematical abilities through experimentation, problem-solving, and design thinking.

For those teachers, administrators, or institutions willing to update their infrastructure, the following are the main STEM lab solutions that will make a difference in 2025.

Modular lab stations

A modern STEM lab is, by definition, very flexible. Modular lab stations are perfect in a school where the space must sometimes be used for robotics, sometimes for chemistry, and sometimes for electronics. These stations usually have moving workbenches, moving storage, and integrated power supplies, making them perfect for interdisciplinary learning.

Why it works:

Efficient use of space

Facilitates teamwork and solo work

Adapting to different grade levels and projects

Robotics & Automation Kits

Being widely accepted in industries, automation is the need of the hour for STEM kits. Robotics kits consist of Programmable Robots, Sensors, Servo motors, and AI Integration kits that allow students to build their robots, program them, and control them.

Our Top Picks:

Arduino-based Robotics Platforms

LEGO® Education SPIKE™ Prime

Raspberry Pi + sensor modules

The kits offer an excellent opportunity to market coding and engineering skills in a manner that is both entertaining and practical.

FDM 3D Printers and Rapid Prototyping Setup

3D printers are no longer a luxury—they remain a must-have. They enable students to build their prototypes, test their mechanical models, and engage in product design. Increasingly, schools are embedding 3D printing into STEM pedagogy so that students can apply their knowledge to solve real-world problems.

Benefits:

Enhances spatial and design thinking

Promotes iteration and creativity

Encourages integration across various subjects (science and art, for instance)

Interactive Digital Boards and Simulation Tools

Chalk and blackboards are a thing of the past. Digital smart boards and simulation software enliven the abstract concepts of STEM, such as chemical reactions or circuit UML diagrams. Teachers have real-time data at their fingertips, can draw on touch screens, and engage students in solving problems together.

Combined with Arduino simulators, circuit design software like Tinkercad, or tools for virtual dissection, it makes the lab intelligent and fun.

IoT- and AI-Based Learning Modules

In 2025, IoT- and AI-based experiments will be part of every competitive mainstream STEM education. Cutting-edge labs are equipped with sensors, cloud dashboards, and microcontrollers to help students build all kinds of smart projects, such as home automation projects, temperature monitoring systems, or AI chatbots.

The solutions prepare the students to think beyond conventional science and prepare tech jobs of the future.

Curriculum-Aligned STEM Kits

Curriculum-aligned STEM kits, thus, remain relevant for teaching. These kits are uniquely designed to meet the lesson plans, experiment manuals, safety instructions, and real-world problem-based learning content required by the curriculum. They are made for specific classes and subjects with which CBSE, ICSE, IB, or state boards can identify.

Features to look for:

Subject-specific kits (Biology, Physics, Chemistry)

Safety compliance (CE, ISO certifications)

Teacher guides and student workbooks

Cloud-Based Lab Management System

Heading into 2025, cloud-based lab management platforms are becoming more and more popular. This allows instructors to track inventory, log student experiments, manage schedules, and upload student reports onto the cloud, thereby cutting down the paperwork and boosting the efficiency of the lab as a whole.

STEM-Learning Corners in Classrooms

These STEM corners in regular classrooms find favor with many schools, especially for the many that do not have the funds for the full-blown labs. Here little places house essential kits, puzzles, experiment tools, and DIY stations where students can entertain themselves exploring topics on their own.

This makes the STEM field much more approachable and far more interesting from an early age.

Conclusion

The year 2025 marks a decision point for investing in Innovative STEM Lab Solutions: choosing to invest is no longer an option but really a must. Through robotics kits, IoT modules, and modular workstations, these solutions pre-emptively prepare students for the future by instilling critical thinking, creativity, and problem-solving abilities.

If your institute is planning a STEM lab upgrade, select the supplier who understands academic requirements and contemporary technology trends. Tesca Global has earned recognition as a name offering second-to-none, affordable, and curriculum-aligned STEM lab solutions customized for schools, colleges, and universities worldwide.

#laboratory equipment suppliers#developers & startups#educational lab equipments#business#news#photography#technology

0 notes

Text

6 Essential Features to Look for in ERP for Pharmaceutical Industry

Not long ago, I met a friend who owns a pharmaceutical company in the United Kingdom. We had planned a casual coffee meetup, but, unsurprisingly, he arrived late. His reason? He was overwhelmed by the complexity of managing various departments and production stages within his pharmaceutical business. That’s when I introduced him to the concept of ERP software for pharmaceuticals—a powerful digital tool that could help streamline his operations and eliminate much of the chaos.

He was intrigued to discover that ERP for the pharma industry can centralize and automate vital processes like inventory, batch production, compliance, and procurement. This sparked his curiosity, and he asked what key features a reliable ERP for the pharmaceutical industry must have.

Here’s a rundown of six essential features that any good pharmaceutical manufacturing ERP software should offer:

1. Formulation and Recipe Management

In pharma manufacturing, formulation management is non-negotiable. ERP for pharmaceutical companies should enable secure documentation of formulas, ingredient-level tracking, and revision controls. Such systems restrict formula access to authorized personnel and incorporate approval workflows, ensuring formulation integrity and traceability. This is particularly important for maintaining consistency in drug production and meeting regulatory guidelines.

2. Batch Management Aligned with cGMP

ERP for the pharma industry must support batch-wise production as per cGMP standards. Whether it’s tablets, syrups, or capsules, the system should manage the full production lifecycle—from batch initiation to completion. This includes material issuance, costing, ticketing, BMR/MBR printing, and SOP execution. An advanced pharma ERP should also enable batch resizing and provide dynamic visibility across the production floor.

3. Quality Control & Regulatory Compliance

A robust ERP for pharmaceutical manufacturing ensures full adherence to standards such as FDA 21 CFR Part 11, EU GMP, and WHO GMP. It should feature built-in QA/QC protocols, audit trails, and electronic signatures. Important modules include non-conformance (NC) handling, CAPA, adverse event reporting, and inspection plans. These features help eliminate errors and establish a quality-first culture throughout the organization.

With documented test outcomes and strict QA/QC controls, ERP for pharmaceutical industry helps manufacturers release only approved products and quarantine or discard non-conforming ones—reinforcing compliance and consumer safety.

4. Lot Traceability for Total Transparency

One of the critical advantages of ERP for pharmaceutical companies is lot traceability. It allows end-to-end tracking of ingredients and finished goods—from sourcing to distribution. In case of product recalls or mock recalls, the system provides a complete log of activities tied to each lot. This function is essential for risk management and maintaining a trustworthy supply chain.

5. Inventory and Material Oversight

An efficient ERP for pharma keeps your inventory under control. It minimizes material wastage, supports scientific inventory monitoring, and reconciles real-time stock data. It enables FEFO-based stock rotation, preventing expired items from reaching the market. Plus, it predicts procurement needs and adjusts inventory levels to match current and future demand. This ensures both cost control and product quality.

6. Procurement and Sales Automation

ERP for pharmaceutical manufacturing companies must support full-cycle procurement and sales functionalities. On the sales side, it should manage opportunities, quotes, orders, invoicing, discounts, and region-specific taxes. In procurement, it should track vendor credentials, select the best supplier based on quality, lead time, and cost, and provide alerts on expiring vendor certifications. Automating the quote-to-receipt process helps speed up sourcing and ensures compliance with purchase policies.

These six core functionalities define the best ERP for pharmaceutical industry. One solution that offers all these features and more is BatchMaster ERP Software for UK Manufacturing Industry. Purpose-built for the pharma sector, this ERP software simplifies complexities and helps manufacturers stay competitive while complying with stringent industry regulations.

Interested in a smarter way to manage your pharmaceutical operations? Click here to explore BatchMaster ERP for Pharmaceutical.

Also Read: How ERP Systems Empower Growth in Pharma Manufacturing

0 notes

Text

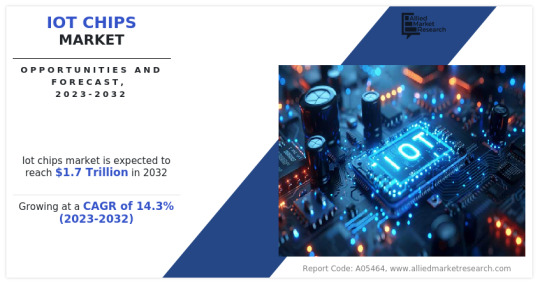

IoT Chips Market to Register Substantial Expansion By 2032

Allied Market Research, titled “IoT Chips Market by Hardware, and Industry Vertical: Global Opportunity Analysis and Industry Forecast, 2023-2032," the IOT chips market was valued at $432.01 billion in 2022 and is estimated to reach $1.7 trillion by 2032, growing at a CAGR of 14.3% from 2023 to 2032.

An Internet of Things (IOT) chip is a small electronic device equipped with sensors, processors, and communication modules that enable it to interact with other devices and systems via the internet. These chips collect data from their surroundings, process it, and transmit it to a central server or other connected devices. They play a crucial role in enabling the functionality of IoT devices by facilitating communication, data processing, and control. IoT chips are integral to various applications, including smart home devices, industrial automation, healthcare monitoring, and environmental sensing, driving the advancement of the IoT ecosystem.

The increase in adoption of IoT devices across various sectors is driven by their ability to enhance efficiency, automate processes, and provide valuable insights through data collection and analysis this increases the IoT chips market demand. In sectors such as healthcare, IoT devices enable remote patient monitoring, medication adherence tracking, and predictive maintenance of medical equipment, leading to improved patient outcomes and cost savings. Similarly, in agriculture, IoT sensors monitor soil moisture levels, weather conditions, and crop health, optimizing irrigation and fertilizer usage to increase yields and reduce resource waste. The widespread adoption of IoT devices underscores the rise in need for IoT chips to power these devices and support their connectivity, data processing, and control functions.

However, cost constraints serve as a significant restraint for the IOT chips industry, manifested through substantial initial investments and high development costs associated with advanced technologies. The development and implementation of IOT chip technology involve high costs, limiting its adoption, particularly among smaller organizations and startups.

Moreover, the expansion of smart infrastructure projects presents significant opportunities for IoT chip manufacturers to supply components for these initiatives. Smart cities, for example, deploy IoT sensors and devices for traffic management, waste management, energy efficiency, and public safety, creating a demand for specialized IoT chips optimized for these applications. Similarly, smart grids leverage IoT technology to monitor and manage energy distribution, reduce outages, and integrate renewable energy sources. With governments and businesses investing in the development of smarter and more sustainable infrastructure, manufacturers of IoT chips have the chance to collaborate with infrastructure providers and solution integrators to furnish the necessary components for these projects, thereby driving market growth and innovation.

The IoT chips market segmentation is segmented based on the basis of hardware, industry vertical, and region. On the basis of hardware, the market is divided into processor, sensor, connectivity IC, memory device, logic device, and others. On the basis of industry vertical, the IoT chips market growth projections is classified into healthcare, consumer electronics, industrial, automotive, BFSI, retail, and others.

On the basis of region, the IoT chips market analysis is analyzed across North America (the U.S., Canada, and Mexico), Europe (the UK, Germany, France, Italy, Spain, and the rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia, and rest of Asia-Pacific), Latin America (Brazil, Argentina, and rest of Latin America), and Middle East and Africa (UAE, Saudi Arabia, Qatar, South Africa, and rest of Middle East & Africa).

The key players profiled in the IoT chips industry include Qualcomm Technologies Inc., STMicroelectronics NV, Samsung Electronics Co. Ltd, Analog Devices Inc., Intel Corporation, Texas Instruments Incorporated, NXP Semiconductors NV, Infineon Technologies AG, MediaTek Inc., and Microchip Technology Inc. These key players have adopted strategies such as product portfolio expansion, mergers & acquisitions, agreements, geographical expansion, and collaborations to enhance their IoT AI chips market penetration.

Key Findings of the Study

The 5G IOT chipset adoption is expected to grow significantly in the coming years, driven by the rise in demand for automated operations by various industries.

The demand for IOT chips in the consumer electronics sector is expected to drive the market.

The IoT chips market share is highly competitive, with several major players competing for market share. The competition is expected to intensify in the coming years as new players enter the market.

The Asia-Pacific region is expected to be a major IOT chips market size owing to significant government investments, a strong focus on domestic technology development, and established players such as Samsung Electronics Co. Ltd and MediaTek Inc in the region.

#iot#iotsolutions#technology#ai generated#iot platform#iotmanagement#iot applications#automation#techinnovation#technologynews#smartcities#techtrends

0 notes

Text

Why a Certification in Medical Coding Is the Fast‑Track Ticket to Remote Healthcare Careers

The healthcare boom isn’t just in hospital wards—it’s online. Certification in Medical Coding sit at the crossroads of medicine, technology, and flexible work. Here’s why earning a certification in medical coding may be the quickest on‑ramp to a location‑independent healthcare career.

1. The Remote‑Ready Nature of Coding Work

Medical coding is fundamentally data interpretation and entry—tasks that require secure software and a stable internet connection, not a physical cubicle. Most electronic health record (EHR) systems and revenue‑cycle platforms are cloud‑based, enabling HIPAA‑compliant access from anywhere.

Stat to note: A 2024 AAPC survey found 62 % of U.S. medical coders now work fully remote or hybrid, up from 34 % in 2019.

3. Certification = Instant Credibility & Higher Pay

Earning industry‑recognized credentials (CPC, CCS, CRC, COC) signals proficiency with ICD‑10‑CM, CPT, HCPCS, and payer guidelines—the core languages of reimbursement. Certified coders command 20–27 % higher median pay than non‑certified peers and often skip entry‑level “apprentice” steps.

4. Accelerated Learning Timeline

Duration: Many reputable programs (including Guardians Ed Tech’s) can be completed in 4–6 months part‑time.

Cost‑Efficiency: Compared with multi‑year allied‑health degrees, a coding certification typically costs 10–15 % as much yet unlocks immediate earning power.

Modular Micro‑learning: Asynchronous video modules and live labs fit around work or family schedules—ideal for career changers.

5. Portability Across Borders & Settings

Because medical coding uses globally harmonized code sets (ICD‑10), certified professionals can serve providers in multiple countries (with minor payer‑specific tweaks). Your credential travels with you whether you live in Mumbai, Manila, or Milwaukee.

6. Pathways Beyond Coding

Certification is a gateway—not a ceiling. Experienced remote coders transition into:

Clinical Documentation Improvement (CDI)

Health‑Data Analytics

Revenue‑Cycle Management Leadership

Compliance & Audit Consulting

Each step up the ladder often retains—or even enhances—your remote flexibility.

7. Work‑Life Autonomy & Inclusivity

Remote medical coding offers:

Flexible shifts (evenings/weekends) for parents or caregivers

Reduced commuting stress & expenses

Opportunities for people with mobility challenges who excel in detail‑oriented digital work

8. How to Fast‑Track Your Certification with Guardians Ed Tech

Enroll in the CPC Mastery Program – live expert‑led cohorts start monthly.

Hands‑On Practice – access to an EHR sandbox with 750+ real‑world case studies.

Exam Readiness Bootcamp – timed mock exams, analytics‑driven feedback.

Job‑Guarantee Pipeline – partner network of 120+ U.S. & global employers seeking remote coders.

Bonus: Guardians students receive lifetime access to quarterly code‑set update workshops—keeping you market‑ready as regulations evolve.

A certification in medical coding is more than a piece of paper—it’s a passport to high‑demand, well‑compensated, and genuinely remote roles in the healthcare ecosystem. With focused training and an industry‑validated credential, you can move from learner to location‑independent healthcare professional in under a year.

0 notes

Text

Photonic Integrated Circuit Market: Key Players and Competitive Landscape

The global photonic integrated circuit market size is expected to reach USD 25.80 billion by 2030, registering a CAGR of 10.8% from 2025 to 2030, according to a new report by Grand View Research, Inc. Photonic IC is an integrated circuit that uses optical wavelength as an information signal and provides multiple integrated photonic functions. Photonic IC, as such, is similar to an electronic IC and can be a viable replacement for it as well as for the copper-based wired transmission. Photonic IC forms an integral part of lasers, optical amplifiers, modulators, and MUX/DEMUX components, which are extensively used in the optical signal processing, optical communication, biophotonics, and sensing applications. The growing demand for sensing and optical devices are expected to fuel the growth of the photonic IC market.

There is an increasing need for cost effective, power efficient, and compact PICs which would further propel the photonic IC market over the forecast period across the mobile broadband Internet access, high-performance computing, datacenter, and enterprise networking, along with metro and long haul data communications, among many others. The increasing adoption of the high-level integrated PICs and application-specific PICs would boost the photonic IC market to strive for greater functionality and new product development across a number of verticals.

The photonic IC market is anticipated to grow substantially due to the continuous technological advancements and the evolving end-user demands. The laser, optical amplifier, and MUX/DEMUX component segments possess enormous growing opportunities, owing to the ability of photonic ICs to incorporate new optical functionalities that can be embedded on a single chip to achieve high efficiency and compactness.

The increasing demand for the optical communication and sensing applications is driving the growth of photonic ICs around the globe with an efficient management of datacenters and long haul networks providing a thriving market for them. Moreover, with the advancements in quantum computing, the adoption of photonic ICs are increasing as they allow multitasking that quantum computing readily requires. Also, the growing adoption of the biophotonic application in medical devices also holds considerable growth opportunities for the photonic ICs market. On the other hand, the high bandwidth and optimum performance requirements of the telecommunication industry, data storage, cloud service providers, and large business enterprises are expected to boost the optical communication and signal processing segments. This market will create many new opportunities culminating in an increased adoption of photonic ICs over the forecasted period.

Request Free Sample PDF of Photonic Integrated Circuit Market Size, Share & Trends Analysis Report

Photonic Integrated Circuit Market Report Highlights

• Based on materials, the III-V Material segment dominated the global photonic integrated circuit market industry with a revenue share of 33.2% in 2024.

• Based on integration process, the hybrid integration segment dominated the global market for photonic integrated circuits in 2024. Some of the common techniques for hybrid integration include selective area growth, die-to-wafer bonding, flip-chip bonding, and others.

• Based on application, the data centers segment accounted for the largest revenue share of the global market in 2024. This is attributed to the performance improvement capacities of photonic integrated circuits (PICs).

• North America photonic integrated circuit market held the largest revenue share of 38.5% in 2024. This is attributed to factors such as growing 5G networks in the region, the large number of data centers operating in North America, the growing demand for the biomedical sector, and the presence of multiple semiconductor market participants in the region.

Photonic Integrated Circuit Market Segmentation

Grand View Research has segmented the global photonic integrated circuit market on the basis of on material, integration process, application, and region:

Photonic Integrated Circuit Material Outlook (Revenue, USD Billion, 2018 - 2030)

• III-V Material

• Lithium Niobate

• Silica-on-silicon

• Others

Photonic Integrated Circuit Integration Process Outlook (Revenue, USD Billion, 2018 - 2030)

• Hybrid

• Monolithic

Photonic Integrated Circuit Application Outlook (Revenue, USD Billion, 2018 - 2030)

• Telecommunications

• Biomedical

• Data Centers

• Others

Photonic Integrated Circuit Regional Outlook (Revenue, USD Billion, 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o Germany

o UK

o France

• Asia Pacific

o China

o Japan

o India

o South Korea

o Australia

• Latin America

o Brazil

• Middle East and Africa (MEA)

o Saudi Arabia

o UAE

o South Africa

List of Key Players in the Photonic Integrated Circuit Market

• Lumentum Operations LLC

• POET Technologies

• Coherent Corp.

• Infinera Corporation

• Intel Corporation

• Cisco Systems Inc.

• Source Photonics.

• Caliopa (Huawei Technologies Co. Ltd)

• EFFECT PHOTONICS

• ANSYS, Inc

Order a free sample PDF of the Photonic Integrated Circuit Market Intelligence Study, published by Grand View Research.

#Photonic Integrated Circuit Market#Photonic Integrated Circuit Market Analysis#Photonic Integrated Circuit Market Report#Photonic Integrated Circuit Market Size#Photonic Integrated Circuit Market Share

0 notes

Text

Computer Aided Engineering Market 2024 : Size, Growth Rate, Business Module, Product Scope, Regional Analysis And Expansions 2033

The computer aided engineering global market report 2024 from The Business Research Company provides comprehensive market statistics, including global market size, regional shares, competitor market share, detailed segments, trends, and opportunities. This report offers an in-depth analysis of current and future industry scenarios, delivering a complete perspective for thriving in the industrial automation software market.

Computer Aided Engineering Market, 2024 report by The Business Research Company offers comprehensive insights into the current state of the market and highlights future growth opportunities.

Market Size - The computer aided engineering market size has grown strongly in recent years. It will grow from $8.97 billion in 2023 to $9.87 billion in 2024 at a compound annual growth rate (CAGR) of 10.0%.The growth in the historic period can be attributed to advancements in computational power, globalization of engineering work, increasing complexity in product design, simulation-driven design, cost and time savings, regulatory compliance requirements, automotive crash testing simulation.

The computer aided engineering market size is expected to see strong growth in the next few years. It will grow to $14.1 billion in 2028 at a compound annual growth rate (CAGR) of 9.3%.The growth in the forecast period can be attributed to rise of industry 4.0 and smart manufacturing, increased complexity in electronics design, focus on sustainability and environmental impact, enhanced human-machine interaction simulations, digitalization of construction and infrastructure, increased use in consumer electronics. Major trends in the forecast period include increased integration of multiphysics simulations, advancements in high-performance computing (hpc), growing adoption of cloud-based cae, focus on user-friendly interfaces and workflows, increased use of generative design, use of virtual prototyping for system-level simulation.

Order your report now for swift delivery @ https://www.thebusinessresearchcompany.com/report/computer-aided-engineering-global-market-report

The Business Research Company's reports encompass a wide range of information, including:

1. Market Size (Historic and Forecast): Analysis of the market's historical performance and projections for future growth.

2. Drivers: Examination of the key factors propelling market growth.

3. Trends: Identification of emerging trends and patterns shaping the market landscape.

4. Key Segments: Breakdown of the market into its primary segments and their respective performance.

5. Focus Regions and Geographies: Insight into the most critical regions and geographical areas influencing the market.

6. Macro Economic Factors: Assessment of broader economic elements impacting the market.

Market Drivers - Increasing automation in the manufacturing sector is expected to propel the growth of the computer-aided engineering market going forward. Automation refers to the development and deployment of technologies for the production and delivery of products and services with little or no human participation. Automation technologies such as computer-aided drafting and computer-assisted N/C tape preparation are now available and widely used in the manufacturing sector to help reverse the troubling trend of declining productivity. For instance, in September 2023, according to the International Federation of Robotics (IFR), a Germany-based professional non-profit organization, the total number of service robots sold for professional use hit 158,000 units in 2022—an increase of 48%. It is recorded that 553,052 industrial robot installations are in factories around the world—a growth rate of 5% in 2022, year-on-year. Therefore, increasing automation in the manufacturing sector is expected to drive the growth of the computer-aided engineering market.

Market Trends - Technological advancements are the key trend gaining popularity in the computer-aided engineering market. Major companies operating in computer-aided engineering are focused on developing new technological solutions to attain a competitive edge in the market. For instance, in June 2021, Siemens AG, a German-based industrial manufacturing company, launched Simcenter Femap, a sophisticated simulation application that allows users to create, update, and evaluate finite element models of complicated goods or systems. Simcenter Femap offers sophisticated data-driven and graphical result visualization and assessment when paired with the industry-leading Simcenter Nastran, resulting in a full computer-aided engineering solution that optimizes the product's performance. When paired with the industry-leading Simcenter Nastran, Simcenter Femap offers sophisticated data-driven and graphical results display and evaluation, resulting in a full CAE solution that enhances product performance.

The computer aided engineering market covered in this report is segmented –

1) By Type: Finite Element Analysis (FEA), Computational Fluid Dynamics (CFD), Multibody Dynamics, Optimization and Simulation 2) By Depolyment: On-Premise, Cloud-Based 3) By End-Use: Automotive, Defense and Aerospace, Electronics, Medical Devices, Industrial Equipment

Get an inside scoop of the computer aided engineering market, Request now for Sample Report @ https://www.thebusinessresearchcompany.com/sample.aspx?id=7941&type=smp

Regional Insights - Europe was the largest region in the computer-aided engineering market in 2023. The regions covered in the computer aided engineering market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East, Africa.

Key Companies - Major companies operating in the computer aided engineering market report are Altair Engineering Inc., Dassault Systèmes SE, ESI Group, Siemens AG, Hexagon AB, Seiko Epson Corporation, Exa Corporation, Bentley Systems Inc., Numeca International, Dell Inc., Aspen Technology Inc., Symscape Pty Ltd, Synopsys Inc., Aveva Group plc, Autodesk Inc., ANSYS Inc., PTC Inc., COMSOL Inc., MSC Software Corporation, Mentor Graphics Corporation, The MathWorks Inc., OpenText Corporation, Siemens Industry Software NV, CD-adapco, ETA Engineering Inc., Ricardo Software, ZWSOFT Co. Ltd., Zemax LLC, Flow Science Inc., GNS Systems GmbH, AVL List GmbH, EnginSoft S.p.A.

Table of Contents 1. Executive Summary 2. Computer Aided Engineering Market Report Structure 3. Computer Aided Engineering Market Trends And Strategies 4. Computer Aided Engineering Market – Macro Economic Scenario 5. Computer Aided Engineering Market Size And Growth ….. 27. Computer Aided Engineering Market Competitor Landscape And Company Profiles 28. Key Mergers And Acquisitions 29. Future Outlook and Potential Analysis 30. Appendix

Contact Us:

The Business Research Company

Europe: +44 207 1930 708

Asia: +91 88972 63534

Americas: +1 315 623 0293

Email: [email protected]

Follow Us On:

LinkedIn: https://in.linkedin.com/company/the-business-research-company

Twitter: https://twitter.com/tbrc_info

Facebook: https://www.facebook.com/TheBusinessResearchCompany

YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ

Blog: https://blog.tbrc.info/

Healthcare Blog: https://healthcareresearchreports.com/

Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

Efficiency and Comfort: Navigating the HVAC Electronically Commutated Motor (ECM) Market

Heating, ventilation, and air conditioning (HVAC) systems are essential components of modern buildings, providing comfort, indoor air quality, and energy efficiency. The electronically commutated motor (ECM) has emerged as a key innovation in HVAC technology, offering enhanced energy efficiency, precise control, and improved performance compared to traditional motors. This article explores the significance of ECMs in the HVAC industry, their diverse applications, and the factors shaping the market landscape.

ECMs, also known as brushless DC motors, are advanced electric motors that utilize electronic controls to regulate speed, torque, and power consumption. Unlike conventional alternating current (AC) motors, which operate at fixed speeds and rely on mechanical brushes for commutation, ECMs employ sophisticated control algorithms and permanent magnets to achieve variable speed operation and optimal energy efficiency.

One of the primary advantages of ECMs in HVAC applications is their ability to modulate airflow and adjust motor speed to match the specific heating or cooling demands of a space. By dynamically adjusting fan speed and airflow based on real-time conditions, ECMs help HVAC systems maintain precise temperature control, humidity levels, and indoor air quality while minimizing energy consumption and operating costs.

Request the sample copy of report @ https://www.globalinsightservices.com/request-sample/GIS21891

Moreover, ECMs offer significant energy savings compared to traditional motors, thanks to their high efficiency, variable speed operation, and advanced control features. By operating at lower speeds when heating or cooling loads are reduced, ECMs reduce energy waste associated with constant-speed motors, resulting in substantial cost savings and environmental benefits over the lifetime of HVAC systems.

In addition to energy efficiency, ECMs contribute to improved comfort and occupant satisfaction by reducing noise levels, minimizing temperature fluctuations, and providing consistent airflow throughout a building. The ability of ECMs to deliver precise and quiet operation makes them well-suited for applications in residential, commercial, and industrial HVAC systems, where comfort, reliability, and performance are paramount.

Furthermore, ECMs support the integration of advanced HVAC technologies such as variable refrigerant flow (VRF) systems, heat pumps, and zoning controls, enabling greater system flexibility, scalability, and responsiveness to changing environmental conditions. By optimizing motor speed and airflow based on real-time feedback from sensors and controls, ECMs facilitate the implementation of energy-efficient HVAC strategies such as demand-controlled ventilation and thermal comfort optimization.

The market for ECMs in the HVAC industry is driven by factors such as regulatory mandates, energy efficiency standards, and technological advancements. As governments and regulatory agencies worldwide continue to prioritize energy conservation and environmental sustainability, the demand for energy-efficient HVAC solutions, including ECMs, is expected to increase, creating opportunities for manufacturers, contractors, and building owners.

Moreover, advancements in motor design, materials science, and electronic controls are driving innovation in ECM technology, leading to smaller, lighter, and more efficient motors with enhanced performance and reliability. Manufacturers are investing in research and development to improve motor efficiency, reduce power consumption, and extend the lifespan of ECMs, further driving adoption in the HVAC market.

In conclusion, ECMs are playing an increasingly important role in the HVAC industry, offering improved energy efficiency, comfort, and performance in heating, ventilation, and air conditioning systems. As building owners, operators, and consumers seek to reduce energy costs, enhance indoor comfort, and minimize environmental impact, the demand for ECMs is expected to grow, driving innovation and investment in this critical component of modern HVAC systems. By navigating the ECM market effectively, stakeholders can achieve greater efficiency and comfort while realizing the full potential of advanced HVAC technology.

0 notes

Text

Photovoltaic Waste Handling: E-waste Management in the UK

Photovoltaic (PV) solar panels are precious assets for the renewable energy sector. From opting for green energy to saving natural resources, solar panels have emerged as an integral power source in the country. The dilemma of photovoltaic waste handling surfaces when the panels reach the end of their cycle. While pounds of solar panels have already been replaced, thousands may end up in the garbage in the coming years. Considering the importance of recovering potential components for remanufacturing and the hazards of improper disposal, it is safe to contact certified recyclers. Recycling solar panel modules is the safest option to avoid environmental toxicity and rising landfills. Are you struggling with non-functional PV panels? We will guide you through the core aspects of managing defunct PV panels. Don't let non-operational panels hold you back.

Overview of PV Module Recycling in the UK

Recycling PV modules is the most convenient option at the end of productive life. Here are the reasons to consider recycling solar panels and avoid heaps of landfills.

#1. PV Panels are Hazardous E-waste

Dr. Vasilis Fthenakis, Department of Earth & Environmental Engineering and Founder and Director of the Center for Life Cycle Analysis (CLCA) at Columbia University, highlights the impact of lead halide perovskite (LHP) photovoltaics on the environment – soil, water, and air. Perovskite PV products contain toxic lead compounds. Exposure to LHP can cause multiple health issues in humans. These crystallographic substances can raise blood pressure levels, cause anaemia, and harm the foetus in pregnant women. Lead ingestion in children can lower IQ, retard physical and brain development, and affect hearing abilities. Recycling is the ideal option for removing solar panels from domestic and commercial premises without risky, accidental contamination. Professional recyclers leverage safe removal methods to prevent exposure of toxic elements to the surroundings.

#2. Recovering Precious Materials

The valuable materials salvaged from the old and inoperable photovoltaic modules can be repurposed for producing new solar panels. The e-waste comprises precious items, especially silicon, silver, and aluminium frames. Moreover, the panels consist of large quantities of glass and plastic, recovered for further use during disassembling. Up to 95% of the glass sheets extracted from the conveyor belt can be recycled. Hence, solar module recycling is a safe method of removing and repurposing valuable assets for future manufacturing.

#3. Alarming Rise of Landfills across the Country

The load of waste is constantly rising across 500 landfill sites in the UK. Every year, over 100,000 tonnes of cheap electronic goods are thrown into waste bins (according to a survey by Material Focus, a non-profit organisation). These items can be recycled to recover the resources for remanufacturing quality products. In the wake of overflowing garbage wastes and shortage of landfill space across the country, it is wise to recycle valued items rather than throwing away.

#4. Economic Growth Prospects of the Solar Panel Recycling Market

The growth of the global solar panel recycling market is estimated at £1.29 billion by 2028. There has been a massive switch to renewable and sustainable energy opportunities in the commercial zones in the last few decades. Large volumes of panels are about to reach the end of life in the next few years. Eyeing the responsible e-waste handling and imposition of WEEE regulations, the recycling industry is booming worldwide, and the UK is not an exception.

Wrapping Up,

Recycling is by far the most effective end-of-life management of PV modules. At least 80-95% of the solar panel components are recyclable, employing safe and permissible extraction methods. When the energy efficiency of worn-out solar panels drops, it is time to replace them with new modules. Rather than discarding it in the garbage, contact us for photovoltaic recycling. At Evolution Solar Recycling, the team of certified recyclers use state-of-the-art equipment for safe PV panel removal to prevent mishaps and accidental exposure to high-risk e-waste chemicals.

0 notes

Text

Active Filters Market is set for a Potential Growth Worldwide

Global Active Filters Market Report from AMA Research highlights deep analysis on market characteristics, sizing, estimates and growth by segmentation, regional breakdowns & country along with competitive landscape, player’s market shares, and strategies that are key in the market. The exploration provides a 360° view and insights, highlighting major outcomes of the industry. These insights help the business decision-makers to formulate better business plans and make informed decisions to improved profitability. In addition, the study helps venture or private players in understanding the companies in more detail to make better informed decisions. Some are the key & emerging players that are part of coverage and have being profiled are Delta Electronics, Inc. (Taiwan), ABB (Switzerland), Emerson Electric Corporation (United States), Helios Power Solutions (New Zealand), Schaffner Holding AG (Switzerland), APAITEK Science & Technology Co., Ltd. (China), Zhuhai Wanlida Electrical Automation Co., Ltd. (China), Murata (Japan), Texas Instruments (United States), Schaffner Holding AG (Switzerland). Get Free Exclusive PDF Sample Copy of This Research @ https://www.advancemarketanalytics.com/sample-report/11910-global-active-filters-market The active filter is an electric circuit that used to change either phase or amplitude of signal characteristics with respect to its frequency. Filter utilizes an operational amplifiers along with several electronic components like resistors, capacitors for the filtering. Active filters are used in communication systems for suppressing noise to improve the unique message signal from a modulated signal. These filters are also used in instrumentation systems by the designers to choose a required frequency apparatus and remove unwanted ones.

The titled segments and sub-section of the market are illuminated below:

by Type (Butterworth, Chebyshev, Bessel, Elliptical), Application (Electric Devices, Machinery, Automobiles, Telecommunication, Others (Audio System and Biomedical Instruments)), Voltage (Low, Medium, High)

Market Trends:

Increasing Usage of Semiconductor Devices

Reduction in the Cost of Power Electronic Semiconductor Devices

Opportunities:

Growing R & D Activities across the Automobiles and Construction Industries

Market Drivers:

Increasing Demand for Consumer Electric Devices

Increasingly Used as UPS Systems for Generating Power Supply

Global Active Filters market report highlights information regarding the current and future industry trends, growth patterns, as well as it offers business strategies to help the stakeholders in making sound decisions that may help to ensure the profit trajectory over the forecast years. Region Included are: North America, Europe, Asia Pacific, Oceania, South America, Middle East & AfricaCountry Level Break-Up: United States, Canada, Mexico, Brazil, Argentina, Colombia, Chile, South Africa, Nigeria, Tunisia, Morocco, Germany, United Kingdom (UK), the Netherlands, Spain, Italy, Belgium, Austria, Turkey, Russia, France, Poland, Israel, United Arab Emirates, Qatar, Saudi Arabia, China, Japan, Taiwan, South Korea, Singapore, India, Australia and New Zealand etc. Have Any Questions Regarding Global Active Filters Market Report, Ask Our Experts@ https://www.advancemarketanalytics.com/enquiry-before-buy/11910-global-active-filters-market Points Covered in Table of Content of Global Active Filters Market:

Chapter 01 – Active Filters Executive Summary

Chapter 02 – Market Overview

Chapter 03 – Key Success Factors

Chapter 04 – Global Active Filters Market - Pricing Analysis

Chapter 05 – Global Active Filters Market Background

Chapter 06 -- Global Active Filters Market Segmentation

Chapter 07 – Key and Emerging Countries Analysis in Global Active Filters Market

Chapter 08 – Global Active Filters Market Structure Analysis

Chapter 09 – Global Active Filters Market Competitive Analysis

Chapter 10 – Assumptions and Acronyms Chapter 11 – Research Methodology Read Detailed Index of full Research Study at @https://www.advancemarketanalytics.com/reports/11910-global-active-filters-market Thanks for reading this article; you can also get individual chapter wise section or region wise report version like North America, Middle East, Africa, Europe or LATAM, Southeast Asia. Contact US : Craig Francis (PR & Marketing Manager) AMA Research & Media LLP Unit No. 429, Parsonage Road Edison, NJ New Jersey USA – 08837 Phone: +1 201 565 3262, +44 161 818 8166 [email protected]

#Global Active Filters Market#Active Filters Market Demand#Active Filters Market Trends#Active Filters Market Analysis#Active Filters Market Growth#Active Filters Market Share#Active Filters Market Forecast#Active Filters Market Challenges

0 notes

Text

Bifacial Solar Market Advanced Technology and New Innovations by 2031 – Jinko Solar Holdings, Trina Solar, LG Electronics, Sharp Corporation

The bifacial solar industry was valued at $8.7 billion in 2021, and bifacial solar market size is estimated to reach $31.1 billion by 2031, growing at a CAGR of 13.6% from 2022 to 2031. Bifacial solar panels are the latest technology designed with high-efficiency solar cells installed on both sides of a module to produce electricity at the same time. It can capture light as it reflects off the roof or ground surface under the panel and absorbs light from rear and front sides, allowing diffused light to be used. Bifacial solar cells use high-watt modules and high-efficiency panels in solar panels and cell development. Rise in demand from commercial & industrial sectors for electricity propels growth of the market, especially during peak times. Increase in demand for solar-based electricity across the globe has led companies to introduce latest advanced solar modules that focus on cost, efficiency, and design. Moreover, reduction of energy cost and rise in affordability has accelerated the bifacial solar market forecast growth.

Get a PDF brochure for Industrial Insights and Business Intelligence @ https://www.alliedmarketresearch.com/request-sample/17339

Feed in Tariff (FiT) is one of the major attractions of taking up renewable energy such as solar panels. The initiative essentially meant that electricity produced by solar panel system was paid by governments to help offset the cost of buying the system. In addition, the European Union initiated “Green Deal” program to reduce carbon emissions and harness residential potential to harvest solar energy. Various other initiatives of the government to improve the environment in rural areas and provide electricity for basic electronic gadgets are the factors that drive growth of the bifacial solar market trends.